If you are looking for an alternative lending method than Peer to Peer finance also known as P2P might be right for you. Keep reading to discover what Peer to Peer lending is, the advantages, disadvantages and how CREDITONLINE can help.

Peer to Peer lending is an alternative lending method that is becoming more popular across the globe and in particular in the UK and Europe. It is a digital lending method that matches borrowers with lenders using an online platform or broker. Unlike traditional lending methods, P2P puts borrowers in direct contact with lenders cutting out the middleman. P2P lending is a great alternative if your business or project doesn’t meet traditional lending methods criteria or is in need of financial support fast.

The application process is fast and straightforward, you will need to complete an online application form with some basic information including details about your business, how long you would like to borrow for and the amount you are looking to borrow. Decisions are made much faster using digital methods of lending and you could have a decision in minutes.

There are many advantages of P2P lending, some benefits include:

Much like any form of lending, there are a small number of disadvantages. These include:

Unlike many traditional lending options P2P finance is available for businesses across a wide range of sectors and locations. There are also not any annual turnover requirements and as long as your business has an established trading history then you can apply for a P2P loan. Before applying you will need to consider what business stage you are at, how much you would like to borrow, interest rates and fees, loan repayments and the time you will borrow for. After making these considerations you will be ready to apply, however we do recommend seeking advice from a financial advisor or specialist before applying.

CREDITONLINE can help with P2P lending in several ways. The first is that we provide the backbone infrastructure for P2P lending businesses. Our technology integrates with all the third parties and services required to conduct everyday business. We offer a completely modular P2P system which means that any modules that you may require will be integrated quickly and efficiently by a team of qualified professionals so that you can achieve your business goals.

CREDITONLINE’s P2P lending software has already been developed and is ready to launch therefore you won’t have to wait to enter the market. Furthermore, surveys have revealed that it costs around £200,000 in software development to start a business. Our startup API costs a fraction of this and can be adapted to meet your needs, therefore cost savings are guaranteed.

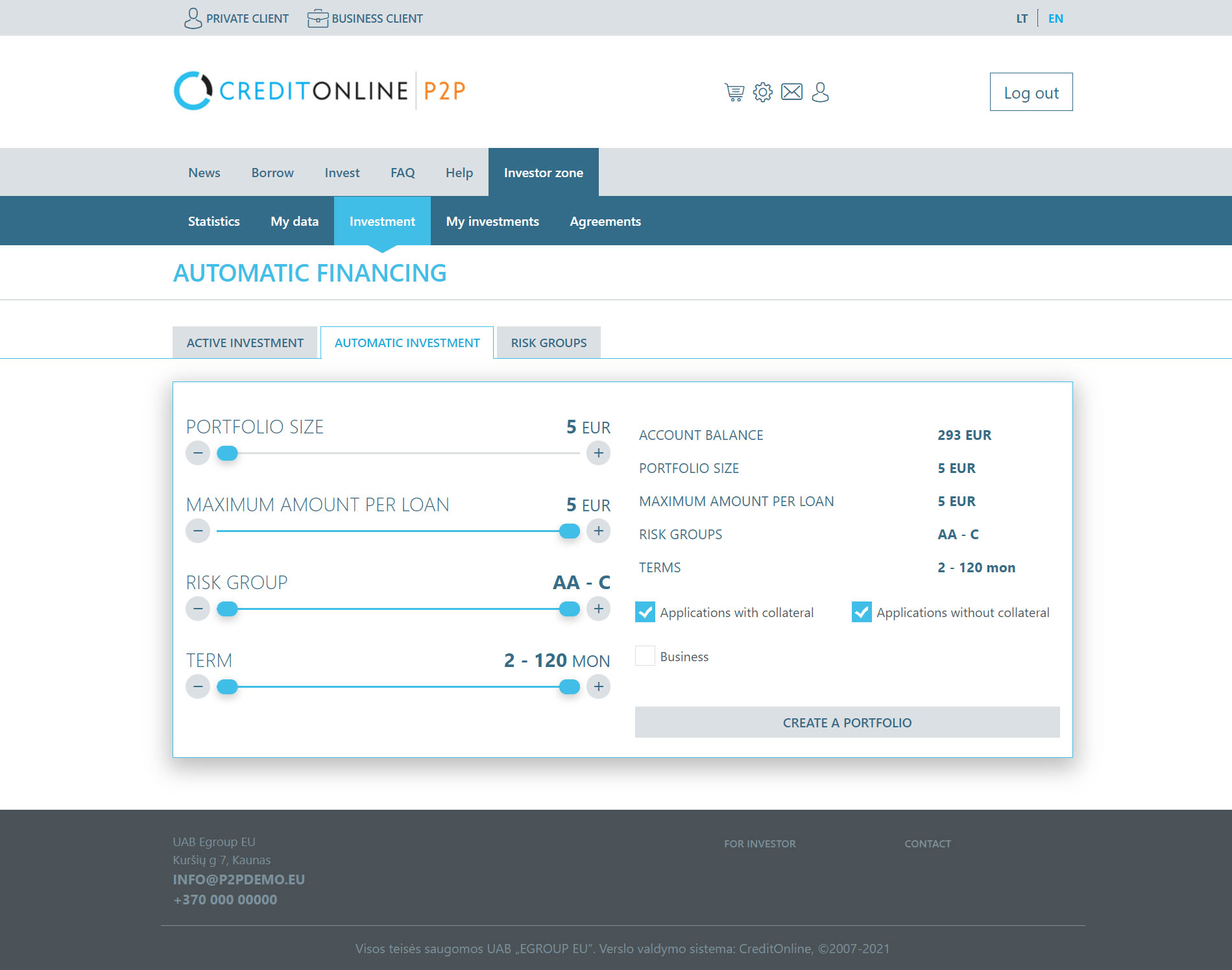

Our system also allows for the P2P loans to be used in a secondary market. This means that our clients are able to sell and buy previous Peers’ loans for an instantaneous return on their investment instead of waiting out the agreed term. Having that as an option also allows us to sell segmented loans and investments instead of forcing our clients to commit to the whole thing.

At CREDITONLINE we offer a seamless P2P platform which can operate with minimal user input. Our system can handle small sums of money such as payday loans all the way to corporate or enterprise clients, so whatever the size of your business our team can help. Contact us to find out more or book a demo.

In the Peer-2-Peer system we have all of the secondary market functionalities, if a client invests into a loan he will have the tools to get his returns back by using one of our secondary markets. On the secondary market, clients are able to sell their investments for less overall value, in exchange for investment holding time.

{kind=link}

{kind=link}

{kind=link}